- To date, China’s retail sales and manufacturing activities point to a broad economic recovery.

- We expect the government to gradually shift from stimulative fiscal and monetary policies in 2021.

- The China–EU investment treaty will likely give European companies greater access to local markets.

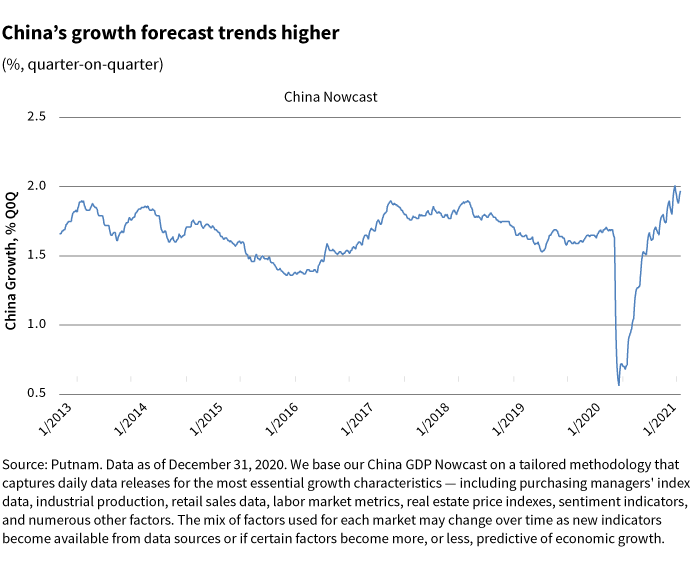

China’s economy is rebounding even as other major economies continue to struggle with the pandemic. The virus spread remains mostly under control.

Retail sales picks up speed

Recovery in economic activity continued in November and December, including retail sales. In addition, over the past few months, the private sector’s industrial production has outpaced industrial production by state-owned enterprises. China’s manufacturing gauges — which moderated last month — currently point to an improving economy. The Caixin China purchasing managers’ index and the official manufacturing Purchasing Managers’ Index (PMI) remain at healthy levels, in our view.

However, we believe there are areas of softness. Industrial production and fixed-asset investment are slowing, and small companies are still lagging in the overall recovery.

China’s CPI inflation turned negative due to a drop in food prices. Now that food prices are easing, we are seeing significant downward moves in headline inflation. We expect inflation to normalize, which is, therefore, not something the People’s Bank of China (PBoC) should worry about in our view. In fact, monetary data continues to indicate a moderation in monetary stimulus. The central bank has cautiously reduced monetary accommodation in some sectors, especially in real estate.

A gradual shift in fiscal and monetary policies

In December, China’s Politburo, the top decision-making body of the Communist Party, and the Central Economic Work Conference signaled an improvement in their assessment of the economy. The Politburo said the government should keep economic growth within a reasonable range in 2021 and work to boost domestic demand. This is a change from the previous meeting, where the emphasis was to attain economic goals, including stimulating the economy.

The central bank has indicated that credit growth will continue to slow in 2021.

We believe this signals the government may be reducing its fiscal and monetary stimulus policies this year. We expect this shift to be gradual and, based on the developments in the rates market, this has already started. The central bank has indicated that credit growth will continue to slow in 2021. We believe a formal rate hike would be too early as the recovery from the pandemic, as well as debt defaults, continue. In the near term, the central bank is likely to keep liquidity flush. First-quarter liquidity needs tend to be higher than usual, especially going into the Chinese New Year.

On the fiscal front, the pandemic relief measure that exempts Social Security fees for small and mid-size enterprises (SMEs) was not extended into 2021. Beijing is also expected to cut subsidies for new energy vehicles by 20% this year.

New investment deal with the EU

In January, China and the European Union (EU) reached an agreement on a new investment treaty, the Comprehensive Agreement on Investment (CAI). Once ratified, CAI will replace the existing bilateral investment treaties between individual EU member states and China with a uniform legal framework.

The agreement is expected to allow EU companies to buy or establish new companies in key Chinese sectors. China has made comprehensive commitments to allow greater market access to its manufacturing sector. Under the country’s new five-year plan, the government has emphasized manufacturing, especially high tech. The CAI includes commitments on fair competition and transparency in subsidies. This type of an agreement can be a reference point for future China–U.S. bilateral negotiations, which are likely to take a different direction under the new Biden administration.

324865

More in: Macroeconomics,