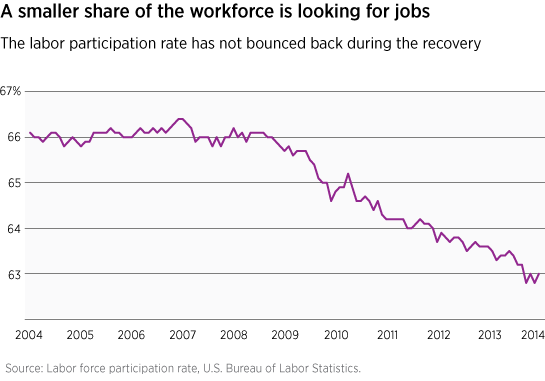

Unemployment continues to drop, but not because a lot of new jobs are being created, as many would hope. Instead, the unemployment rate is dropping primarily due to a declining labor participation rate.

This remains a cause for concern for us because of what it could mean for inflation.

The Fed, under Chairman Ben Bernanke, believed that an easy money policy — which tapering will not eliminate this year, but only gradually reduce — would generate enough cyclical dynamism to counteract any negative effects of the prolonged downturn. While the economy has remained in recovery, GDP growth has been less than dynamic.

Furthermore, the Fed continues to believe that the non-accelerating inflation rate of unemployment (NAIRU) — the rate to which unemployment can fall without triggering wage inflation — is around 5.6%. However, our research suggests, and some institutions share the opinion, that the NAIRU may be significantly higher than this, primarily because of various structural problems hampering the labor participation rate.

Generally speaking, investors believe wage inflation could become a problem sooner than expected.

As the unemployment rate moves downward, if wage inflation develops earlier than the Fed is anticipating, we could see the central bank reduce its stimulus efforts much earlier than the markets are currently forecasting.

We do not see this eventuality coming to pass during this winter, but it could be a development that raises significant concerns for the Fed and the markets later in 2014.

Read Putnam’s Fixed Income Outlook.

More in: Fixed income, Outlook