Ask a manager of a multi-asset portfolio: What important statistic gets too easily overlooked? The answer will likely be: the correlation between stocks and bonds.

This one statistic provides a breadth of information about the value of diversification at any point in time.

However, it is difficult to forecast. As with returns, historical information is the only guide. Keep in mind, though, that for the purposes of risk management and portfolio construction, yesterday may be largely irrelevant.

A tale of two periods

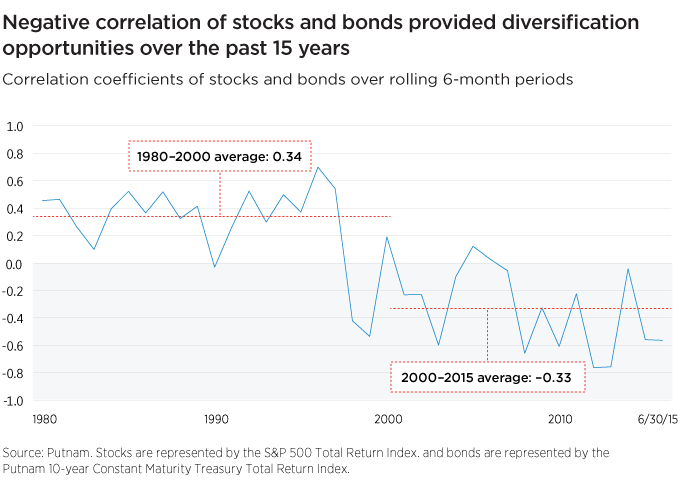

Over the past 15 years, we have enjoyed a period in which the price correlation between stocks and bonds has mostly been quite negative. Simply put, when one zigs, the other zags.

In contrast, however, during the 20 years prior to 2000 — during the equity bull markets of the 1980s and 1990s — this correlation was mostly positive.

Why correlations changed

There are a number of theories as to why the relationship changed, but most have focused on the risk of inflation in the 1980–2000 period and the risk of deflation in the post-2000 period.

The question now is, will stock-bond correlation in the coming years return to the level of the 1980s and 1990s, or remain like 2000–2015, and warrant a bond allocation?

The Fed may be a menace

Today, many point to the Fed’s outlook for raising interest rates in coming years and anticipate that it will cause strongly negative returns for bonds of all kinds. In addition, as the Fed’s confidence grows that we are moving back toward its inflation target, the correlation between stocks and bonds could again become sustainably positive, taking away the diversification benefit.

Bonds matter to diversification

We have a different view. We do not anticipate negative results for bonds or the loss of the diversification benefit any time soon.

Across the bond market, we continue to find pockets of opportunity that we think can persist for a while longer. Both prepayment and credit risk of all kinds still appear somewhat attractive. And if the next tightening cycle plays out at all like the last one in 2004–2006, longer-dated bonds could still provide some ballast to riskier assets in portfolios. We find positive carry, measured simply by the slope of the yield curve, to be strongly associated with positive excess returns to duration exposure.

Weighing the risks of inflation and deflation

At the same time, we doubt that the world has moved far enough away from deflation to warrant a shift back to a positive correlation between stocks and bonds.

Also, while we have concerns about wage inflation in the United States, inflation trends are influenced by the global setting. There is plenty of excess labor and manufacturing capacity around the world that can help restrain inflation. In addition, the tremendous amount of debt globally provides a deflationary force. The result is that bonds continue to help diversify multi-asset portfolios and bring overall volatility down.

297356

More in: Asset allocation