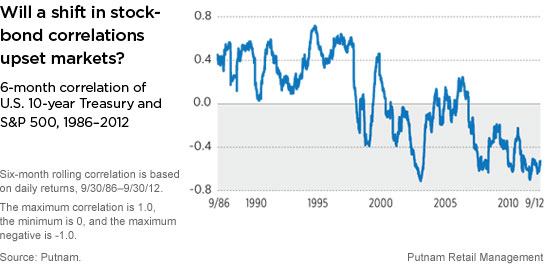

We are watching for a possible shift, although it is not yet evident, in the correlation between stocks and bonds, which measures how similarly or differently these asset classes perform. For the past 10 years, this correlation has been consistently negative — when stocks have struggled, bonds have done well, and vice versa (a correlation approaching the maximum negative of -1.0 means that historical returns of two asset classes have often moved in opposite directions). This dynamic has been especially useful for balanced investors, as the diversification benefit to owning bonds has been dramatic.

This strong negative correlation has not always held, however. In fact, for many years before 1997, the opposite was true — bonds and stocks tended to show a positive correlation (a positive correlation near 1 indicates similar return paths).

While this metric remains negative, we believe that a shift back toward historical correlation patterns would present a significant disruption to financial market conditions. Consider government bonds like U.S. Treasuries. Today, most investors agree that return prospects for these bonds are relatively unattractive. Nevertheless, allocations to interest-rate-sensitive bonds have been growing for years, largely because their negative correlation to stocks constitutes a significant benefit to a balanced portfolio.

Should that attribute weaken, the case for allocating to interest-rate-sensitive bonds weakens as well. At minimum, this would elevate the volatility of balanced portfolios. More likely, it would prompt many investors to shift out of bonds, which could result in a rapid jump in bond yields.

More in: Asset allocation, Outlook