- In the second quarter of 2020, home ownership increased at its highest rate since the third quarter of 2008, according to the U.S. Census Bureau.

- While tight inventory typically drives up home prices, affordability has increased due to low mortgage rates, which are a key driver of home ownership.

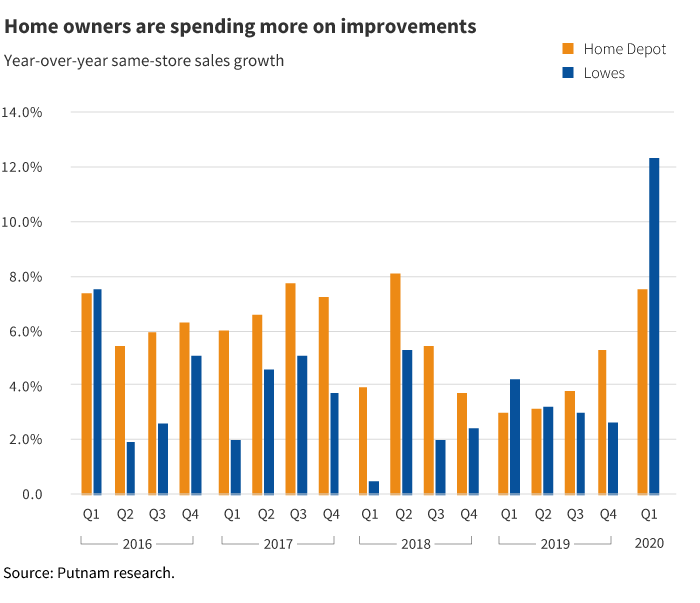

- In July, consumers increased spending on home improvement by 20% year over year according to Bank of America credit card data.

We believe that continued demand for products, services, and supplies bodes well for home improvement retailers.

As the economy continues to be challenged by the COVID-19 pandemic, we are seeing two notable trends in the U.S. housing industry. More people are buying houses and existing homeowners are spending more to improve theirs. It raises an interesting question: Is this happening despite the pandemic or because of it?

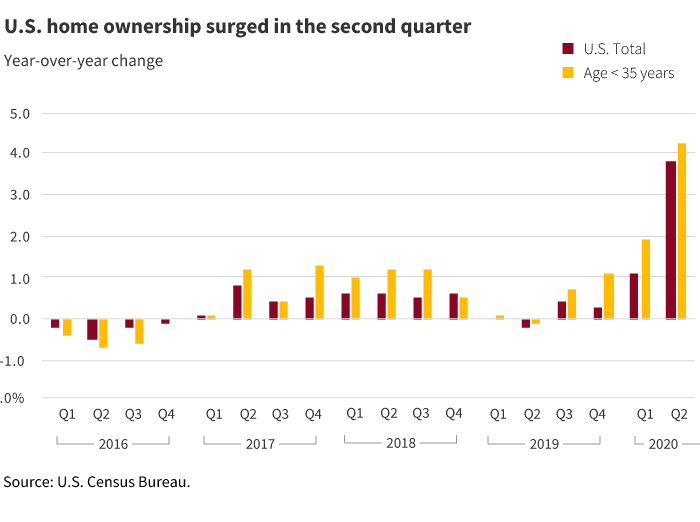

Ownership among younger buyers is at a 12-year high

In the 2020 second quarter, home ownership increased to 67.9%, according to the U.S. Census Bureau. This was the highest rate since the third quarter of 2008. People under age 35 have been active, with home ownership for this group rising to 40.6%, a level not seen since before the global financial crisis. This is quite possibly because of the pandemic, as buyers may be compelled to move from crowded cities and seek homes in suburbs.

The inventory of U.S. homes remains below the long-term average. Homes available for sale as a percentage of housing stock is currently 1%, versus a 20-year average of 1.6%. While tight inventory typically drives up home prices, affordability has increased due to low mortgage rates.

More time at home drives do-it-yourself spending

In 2020, most of us are spending significantly more time in our homes, which, not surprisingly, has increased interest in home improvement projects. In May and June, retail sales of building materials and garden supplies experienced growth in the high teens versus low single-digit growth in the 2020 first quarter. We believe the solid demand from homeowners for products, services, and supplies bodes well for many stocks in the consumer sector, particularly home improvement retailers and their suppliers.

Investment opportunities

In July, home improvement spending increased 20% year over year according to Bank of America credit card data. Stocks that we believe could potentially benefit include:

Home Depot (HD) and Lowe’s (LOW). We expect strength from home improvement retailers for the second quarter. In our view, unlike many retailers, these businesses are somewhat insulated from the “Amazon effect” — the pressure placed on traditional businesses from online competition. We believe they can withstand this threat due to the specialized nature of their products and the services.

Sherwin-Williams (SHW). Paint manufacturers may be another beneficiary of consumer spending on home improvement. For example, Sherwin-Williams has put considerable research and development into tailoring its products, retail stores, and ordering systems.

Keeping an eye on earnings

Businesses enter the third quarter with great uncertainty around the outlook for economic recovery and COVID-19. As companies report quarterly earnings, analysts across our global equity research team have ongoing discussions with company management teams. They are gaining insights and stress-testing their models of earnings and balance sheets. As always, this kind of fundamental research is the key driver of security selection for our portfolios.

322947

ICE Data Indices, LLC (“ICE BofA”), used with permission. ICE BofA permits use of the ICE BofA indices and related data on an “as is” basis; makes no warranties regarding same; does not guarantee the suitability, quality, accuracy, timeliness, and/or completeness of the ICE BofA indices or any data included in, related to, or derived therefrom; assumes no liability in connection with the use of the foregoing; and does not sponsor, endorse, or recommend Putnam Investments, or any of its products or services.

As of June 30, 2020, Home Depot accounted for 1.95% of the Putnam U.S. Research strategy and 1.22% of the George Putnam Balanced strategy, and was not held in Putnam Global Core Equity strategy. Lowe’s accounted for 1.77% of the Putnam Global Core Equity strategy, and was not held in the U.S. Research strategy or George Putnam Balanced strategy, and Sherwin-Williams accounted for 1.70% of Putnam Global Core Equity strategy and 0.31% of the George Putnam Balanced strategy. It was not held in Putnam U.S. Research strategy. The companies presented as investment examples represents the consumer discretionary securities deemed most relevant to the applicable home improvement theme being discussed. Investment themes selected based on high conviction ideas and are determined by Putnam’s Equity Research team. Current investment themes and investment examples were selected without regard to whether such themes, or relevant securities, were profitable and are intended to help illustrate the investment process. The inclusion of company information should not be interpreted as a recommendation to buy or sell or hold any security. It should not be assumed that investment in the securities mentioned was or will be profitable. Holdings are for a representative account and are shown for illustrative purposes only. Each account is managed individually. Accordingly, account characteristics may vary.

This material is a general communication for informational and educational purposes only. It is not designed to be a recommendation of any specific investment product, strategy, or decision, and is not intended to suggest taking or refraining from any course of action. The material was not prepared, and is not intended, to address the needs, circumstances, and objectives of any specific institution, plan, or individual(s). Putnam is not providing advice in a fiduciary capacity under applicable law in providing this material, which should not be viewed as impartial, because it is provided as part of the general marketing and advertising activities of Putnam, which earns fees when clients select its products and services. The views and strategies described herein may not be suitable for all investors. Prior to making any investment or financial decisions, any recipients of this material should seek individualized advice from their personal financial, legal, tax, and other professional advisors that takes into account all of the particular facts and circumstances of their situation. Representative account data in this report is for illustrative purposes only. Generally, the representative account is selected based on the account that has the longest track record or that is most representative of the intended strategy taking into consideration the account with the least investment restrictions, the size of the account, and/or most relevant and applicable to the prospective client. Representative accounts may change over time. Predictions, opinions, and other information contained in this material are subject to change. Actual results could differ materially from those anticipated. All investments involve risk, and investment recommendations will not always be profitable. Putnam Investments does not guarantee any minimum level of investment performance or the success of any investment strategy. Investing entails risks, including possible loss of principal. Past performance is no guarantee of future results.

More in: Equity,