Two weeks after Election Day, we believe the markets have a lot more clarity. From a political standpoint, former Vice President Biden has secured enough electoral college votes to be named president-elect and the Democrats have retained control of the House of Representatives. From a pandemic standpoint, data from two vaccine trials so far have been extremely positive.

Despite these developments, some uncertainties remain: the lack of a concession from President Trump, and which party will control the Senate, an outcome to be determined by two run-off elections in Georgia. In our opinion, both of these uncertainties are currently being priced in volatility markets:

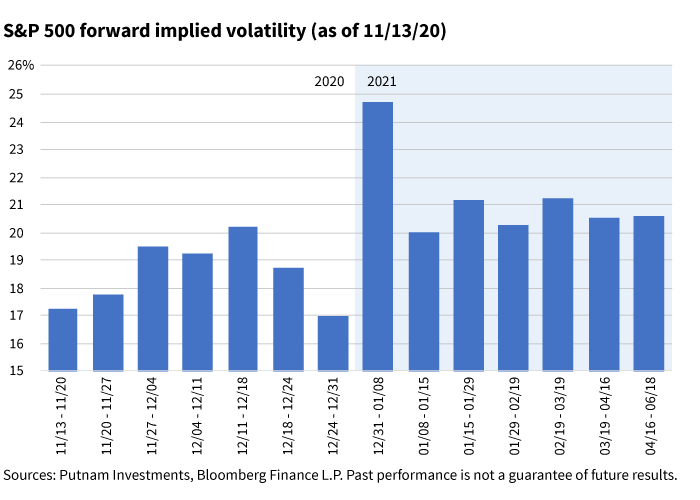

Looking at the forward implied volatility from S&P 500 options contracts gives us a granular look at how the market is pricing risk on a weekly basis. From the chart above, we can see two implied events in the immediate future: one during the week of December 11–18, 2020, and one during the week of December 31, 2020–January 8, 2021. The small risk event (< 1 volatility point) during the week of December 11–18, 2020, is likely the meeting of the Electoral College on December 14. At this point, we feel it is quite a long shot that the Presidential election results would be overturned. The large risk event (~ 4 volatility points) during the week of December 31, 2020–January 8, 2021, is likely the Senate run-off elections in Georgia. They are scheduled for January 5, 2021, and it is possible for the Democrats to take control of the Senate if they win both run-off votes. This would give Democrats control of both houses of Congress and the presidency. The relative size of the volatility premiums indicates to us that markets view the Georgia Senate elections as the more plausible risk event.

The S&P 500 Index is an unmanaged index of common stock performance.

324100

More in: Equity