- Most executives at publicly traded companies have a significant portion of their annual compensation tied to performance goals.

- However, gauging the effectiveness of incentive compensation can be difficult for management, boards, and investors, who must evaluate the metrics that best correlate with improved business outcomes or share price performance.

- While many companies use total shareholder return as the metric for incentive plans, other measures might highlight different and important aspects of management success.

For investors concerned about corporate governance issues, the structure of management incentive compensation has become a prominent consideration. Still, we do not have a complete understanding of the linkages between pay structures and company performance. While many companies have moved to incorporate total shareholder return (TSR, or stock price appreciation plus dividends) into their incentive metrics, the use of this metric alone does not necessarily ensure alignment between management and shareholders.

“Show me the incentive and I will show you the outcome.”

– Charlie Munger

Finding the right compensation measures

Many publicly traded companies, including those listed in the S&P 500 Index, link a part of their executives’ annual compensation to performance goals, including TSR, return on invested capital (ROIC), earnings per share (EPS), and revenue growth. These incentive plans provide shareholders insight on how management pay is aligned with company performance.

Long-term incentive plans (LTIPs) most frequently use TSR as a performance metric, followed by return on capital and EPS. Short-term incentive plans (STIPs) often focus on operating income, or revenue. More than 80% of companies in the S&P 500 used performance awards in 2015, compared with about 50% in 2009, according to a report from Stanford Graduate School of Business (CEO Compensation Data Spotlight). In 2016, more than 90% of these companies disclosed LTIPs, company filings show.

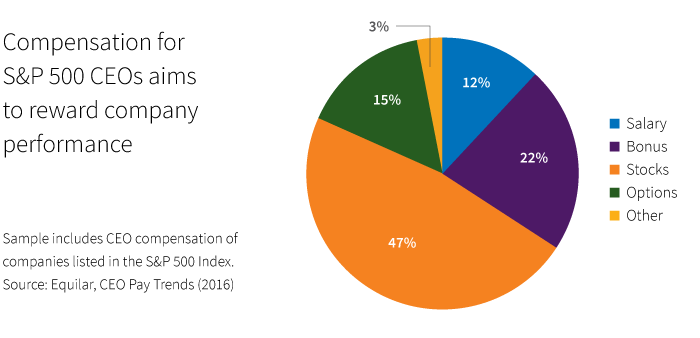

Performance-based pay accounts for the majority of CEO compensation for the average S&P 500 company. Only 12% of compensation is salary, 22% comes from short-term incentives such as annual cash bonuses, and more than 60% of total compensation is from long-term incentives such as stocks and options, the Stanford report shows.

Does stock performance equate with company performance?

Investors may assume that companies should link executives’ pay with share price performance, and indeed, total shareholder return is the most popular metric in incentive plans. According to the Stanford study, 57% of companies in the S&P used it in incentive pay. However, there is little empirical evidence that shows a relationship between TSR-based incentive plans and company performance. What’s more, company management doesn’t directly control the performance of their stock, especially in the short term, whereas the CEO has direct responsibility for the stewardship of a company’s capital and has direct influence over operating results.

It’s tempting to think that stock performance and management performance are one and the same, and over the long term the two should be closely linked. But there is often a disconnect between long-term total CEO pay and long-term shareholder returns. One recent MSCI study shows that there is little relationship between CEO pay and shareholder returns, even over a 10-year period.

There are several possible explanations for this. Perhaps some stocks were impacted by external factors like commodity prices or takeover valuations in their sector. Perhaps some CEOs created or destroyed value in a way that did not directly impact shareholder returns. And let’s not forget the likelihood that some of these outcomes involve luck, where some CEOs were unintentionally overpaid and some underpaid versus the 10-year arc of their companies’ TSR.

When it comes to incentives, one size does not fit all: Each sector of the market has different exposures to key performance indicators, and executive compensation should be able to reflect these differences. Yet the disconnect between long-term total CEO pay and long-term shareholder return indicates that important questions remain.

Research continues on an important governance issue

It’s important for investors to be able to understand how a company’s performance relates to its executive’s pay. As compensation measures become more complicated, the assessments have turned increasingly interesting and nuanced. For example, a metric that works in one industry may not be tied to value creation in another industry. In general, investors would be wise to pay attention to how capital stewardship impacts both company and executive performance, and should aim to understand the rationale and measurements behind incentive awards. Incentive compensation measures reveal a lot about internal company priorities in a way that sometimes amplifies and sometimes contradicts the company’s stated mission.

Given these complications, in the short term, Charlie Munger’s claim might not be so obvious: We can’t always directly tie an incentive to an immediate outcome. The power of incentives becomes more apparent over the long term. Viewing executive compensation in this light can help us to identify organizations that are best aligned with true long-term value creation for their investors and other stakeholders.

309024

More in: Equity, Sustainable investing