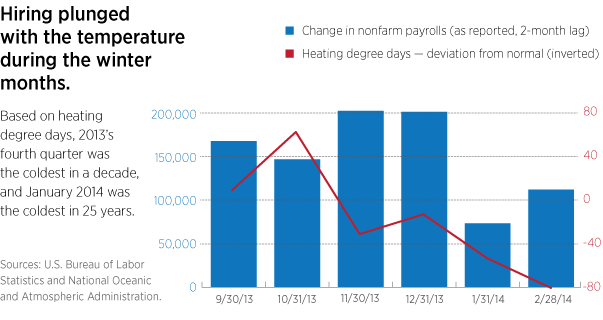

The polar vortex that spread across great swaths of North America several times this past winter numbed economic data. One way to understand the impact of winter is to analyze heating degree days. These calculations measure the energy consumption required to heat buildings and appear on the monthly utility bills of many homeowners. Based on this statistic, it was the coldest fourth quarter in a decade and the coldest January in 25 years.

Our optimism continues

At the start of the year, we anticipated a gradual broadening of the recovery, with enough impetus to lift the GDP growth rate back to its post-financial-crisis average of 2.5% to 3%. One of the key ingredients in this outlook was the expectation for job creation to continue near the pace of 200,000 positions per month, which it had averaged since early 2011. When job creation slowed substantially in December and January, stock prices and bond yields both became more volatile. The housing market also showed weakness, as building permits, new home sales, and construction activity felt winter’s chill.

We dove deeper into the data to make sure our outlook remained intact. Following some of the coldest periods in December and January, the job numbers began to snap back to nearly 200,000 for both February and March. In addition, purchasing managers’ surveys, which measure business spending on equipment, were more stable. This combination of factors persuades us that the recovery has not been thrown off track. As the weather itself improves, the data should improve also.

288254

More in: Outlook