U.S. GDP growth during the recovery, underway since the middle of 2009, is among the weakest in recent history. It has averaged a little over 2% for the past four years, well below the previous long-term trends of 3% to 3.5%. Amid this slow recovery, investors have been looking for the economy to shift to a faster gear, what economists sometimes refer to as “escape velocity.”

Such a shift appeared likely in mid 2011, until the escalation of the European sovereign credit crisis, Japanese tsunami, and U.S. credit downgrade triggered turmoil. Hopes also increased in 2012, before Europe again tottered on the edge of a deleveraging crisis and the U.S. government went to the precipice of the fiscal cliff. In both cases, the pace of GDP growth declined, bordering on what might be called “stall speed.”

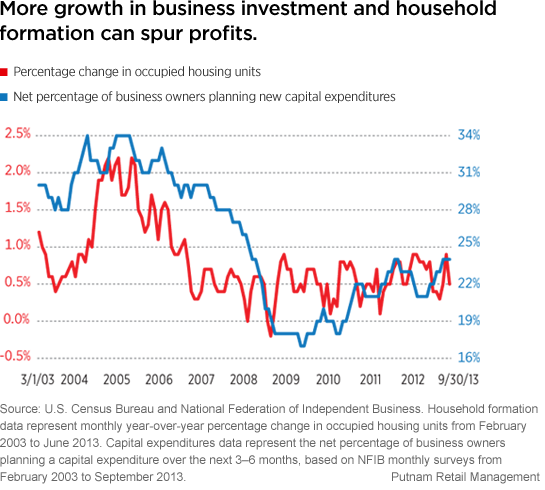

Higher profits may depend on stronger growth

While the difference between a 2% and a 3% growth rate may not seem like much, it influences what has historically been a strong relationship between real GDP growth and corporate profits. Over the past five quarters, the revenue growth of S&P 500 companies has barely been above 1%, providing little impetus to bottom-line earnings growth.

The good news is that as we approach 2014, an economic reacceleration seems to be on track. At the same time, the threat of global macro risks of recent years, including European sovereign debt and China’s economic slowdown, is shrinking. At the moment, it is important that U.S. politics does not derail the recovery.

Consumer spending depends on new households

The thrust that could push the economy higher may come from the pent-up demand of households and businesses. Household formation fell sharply during this downturn and only began to pick up again in 2012. Over the past couple of years, more people have felt confident to move into their own apartments or to buy houses. These are the preconditions for future growth in consumer spending, as it costs money to furnish or update houses, and to raise families.

Businesses need to feel more confident

Businesses, similarly, have been slow to ramp up capital expenditures and hiring, although these trends are at least moving in a positive direction. The big question today is whether CEOs and CFOs perhaps see the same signals that the Fed perceived. Do they have high expectations, warranting greater investment and hiring, or do they detect weakness that calls for continued caution?

We believe it would take additional spending, driven by rising expectations, for the economy to provide the setting for stronger earnings growth.

Read Putnam’s fourth quarter Capital Markets Outlook.

284525

More in: Asset allocation, Equity, Outlook