As the Federal Reserve plots its actions and communications strategy for the gradual normalization of monetary policy, fixed-income investors face the challenge of anticipating the future course of interest rates.

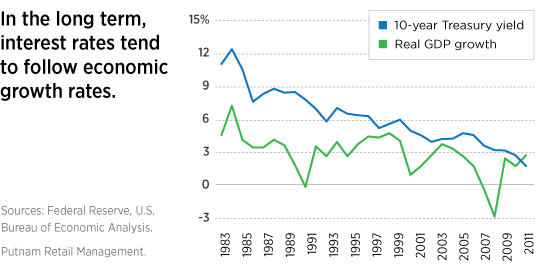

Economic growth influences interest rates

The long-term “equilibrium” interest rate of an economy is intimately linked to the economy’s overall growth potential when it is free of distortions, such as recessions or the energy supply shock of the 1970s, or the demand shock that followed the financial deleveraging crisis of 2008. The term “equilibrium” does not imply that these rates prevail most of the time. In fact, there can be large deviations from the equilibrium.

The relationship between economic growth and interest rates flows from demand for money. When economic activity accelerates, there is more demand for capital, causing the price of money — or interest rates — to increase. When the economy is sluggish or contracting, the price of lending decreases.

Understanding growth depends on analyzing labor

To calculate an economy’s growth potential, the most important variables involve labor — how much labor is available and how much capital is available for labor to utilize, which determines overall labor productivity. An economy’s growth rate is driven primarily by the change in labor supply and the change in labor’s productivity.

The United States faces growth challenges

When economic experts look at these factors in the recent history of the United States, most conclude that the potential U.S. growth rate is declining. That’s because the labor force is growing more slowly than it did in recent decades and because productivity has also been disappointing. We’ll look at these factors in subsequent posts.

If this view is correct, potential U.S. economic growth will be lower in the future than the approximate 3% level of the 30 years prior to the 2008 crisis. This would suggest that interest rates across the term structure would also be lower in the future than in recent decades. In turn, this outlook would have major consequences for income planning strategies.

Of course, rates would still likely be higher than current levels, which are being held below equilibrium by the Fed’s asset purchase programs.

284639

More in: Fixed income, Macroeconomics