- 2017 and 2018 saw relatively small movements in Treasury yields

- Yields remain likely to rise in the medium term

- Active strategies can help to offset the risk of rising yields

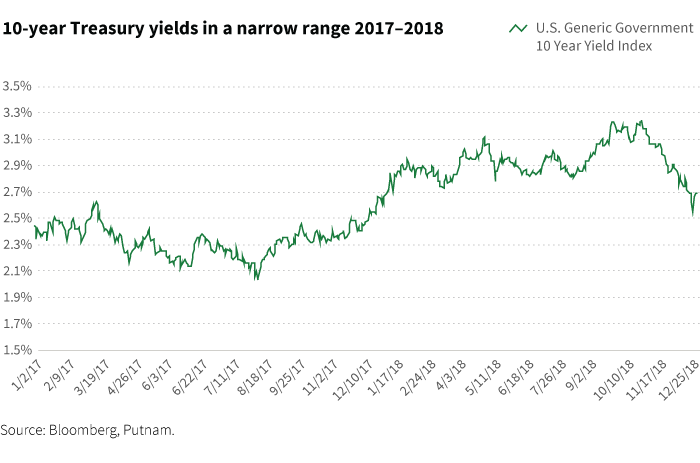

Yields have moved within a narrow range for two years

Since the start of 2017, the U.S. 10-year Treasury has traded in a range with yields of 2.04% to 3.24%. Although this range is not particularly wide for a two-year period by historic standards, the changes in trends during this period were significant: a drop of 58 basis points (bps), a rise of 119 bps, and a drop of 68 bps. Given the high level of interest-rate sensitivity in Treasuries and investment-grade bonds, investors have felt these rate moves in their portfolios.

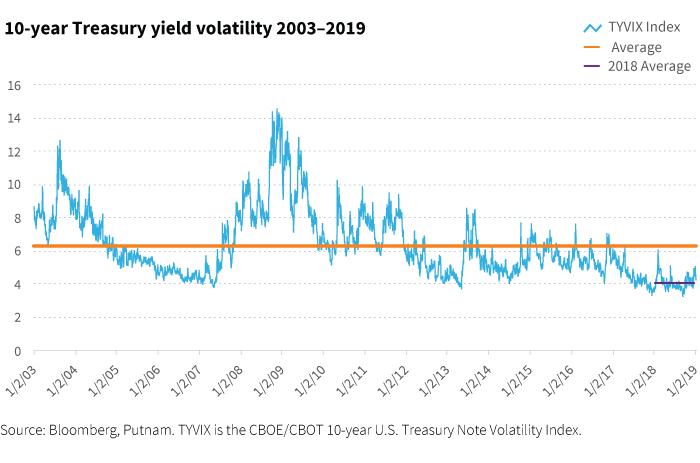

Yield volatility actually fell during 2018

Over the past couple of years, the volatility environment has been historically low. Most people associated the low-volatility environment with equity markets, but low volatility has been a common characteristic across a number of asset classes. These asset classes include fixed income, and the more interest-rate-sensitive areas of fixed-income markets.

To see this low level of volatility, consider the CBOE 10-YR U.S. Treasury Note Volatility Index (TYVIX). Just as the VIX Index measures the volatility of the S&P 500 Index, TYVIX measures Treasury note volatility. In 2018, even as financial advisors and asset managers gave warnings about the risks of rising rates, the actual volatility of the U.S. 10-year Treasury was well below average. Since the TYVIX has been tracked, the long-term average is 6.30. The 2018 average was 4.04. It was even lower than the below-average rate of 4.50 in 2017.

Active duration may be helpful if yield volatility reverts to more normal levels

Our view is that rates are biased upward over the medium to long term. However, as yields remain low around the globe, the landscape and dynamic may keep the U.S. 10-year lower for longer. In other words, the low volatility of the past couple of years could persist.

These two juxtaposing forces may create a trading range for the U.S. 10-year in the interim. If TYVIX moves to more normal levels, a wider range could be established. Investment managers can take advantage of trends within this range actively, rather than having a structural duration position.

We believe that diversifying away from interest-rate risk within fixed-income sectors is a strategy to help neutralize this risk over the medium term. Examples of ways to do this include allocations to non-traditional bond portfolios or to multi-asset strategies capable of tactical positioning in rates.

316196

More in: Fixed income