- The president has made proposals for individual income tax increases

- As proposed, we would not expect the modest increase in the top federal income tax bracket to have a large impact on taxable equivalent yields

- We would not expect muni/U.S. Treasury yield ratios to move abruptly with the proposed changes to the top income bracket

The Biden administration’s latest fiscal proposal, the American Families Plan, released in late April, calls for increased spending and proposes tax increases for higher-earning households.

The plan would increase the highest marginal income tax rate from 37% to 39.6% — the level that existed prior to the Tax Cuts and Jobs Act of 2017 (TCJA). The 39.6% tax rate has also been the most common maximum federal individual tax rate over the past 30 years.

These moves follow the administration’s proposal for the American Jobs Plan, which proposed infrastructure improvements along with an increase in the corporate tax rate (from 21% to 28%), among other tax changes.

Tax rate increases for individuals are rare

Increases to the top federal individual tax rates have been uncommon in the past 30 years. There have only been two notable top individual tax increases since 1990 (1993 and 2013). In both cases, when the top individual tax rate increased, municipal bond funds experienced inflows in the year, or several years, following the tax increase.

General outlook for muni yields and Muni/UST ratios

We do not expect a material shift in tax-exempt muni yields in the near term because of the proposed change in top federal individual income tax rate. This is largely due to the current relative richness of tax-exempt munis and the modest size of the increase in the top tax rate.

We anticipate:

- The muni index (Bloomberg Barclays Municipal Bond Index) taxable-equivalent yield may increase slightly (to 1.77% from 1.69%) under a higher individual tax rate than the current top tax rate

- Tax-exempt munis could remain richly valued versus other fixed-income alternatives

The correlation between muni/U.S. Treasury ratios (a measure comparing yields of municipal bonds with Treasury bonds of the same maturity and quality) and top individual tax rates is weak.

Consequently, we do not expect the potential proposed federal income tax increases to cause large ratio changes in the near term. Muni-ratios remain very rich on a historical basis.

A deeper dive on muni yields

One key valuation metric for munis is the taxable-equivalent muni yield. This data helps us frame the attractiveness of tax-free munis in context with other, taxable fixed-income alternatives.

We don’t expect any material changes in muni yields in the near term for several reasons:

- The proposed increase in the maximum federal individual tax rate is speculated to be modest (rising from 37% to 39.6% for incomes higher than $400,000)

- The proposed increase would only have a small impact on tax equivalent muni yields (see chart below)

-

-

- In the illustration, the two red-striped columns represent Muni index, muni taxable equivalent yields (TEY) at different maximum federal individual tax rates

- Muni Index TEY at the current 37% maximum income tax rate (+3.8% Medicare tax) is 1.69%

- Muni Index TEY at the proposed speculated 39.6% maximum federal income tax rate (+3.8% Medicare tax) is 1.77%

-

- This small change is due to a modest move in tax rates and, more importantly, the current low level of muni yields

- The fairly significant proposed change in the capital gains tax for incomes above $1 million could increase muni demand, as investors look to shift assets into munis to reduce tax liability

We are monitoring additional factors

Other factors which could alter the muni market supply/demand landscape include:

- A change to the state and local tax (SALT) cap, which could influence investor appetite for munis. This could indirectly alter muni taxable-equivalent yields. We would note that a repeal of the SALT cap would be expensive; some estimates range up to $400B over the next four (4) years

- Changes to the capital gains/dividend tax rate, which could motivate investors to invest in tax-exempt munis to reduce their tax liability. The Biden Administration is proposing a 39.6% capital gains tax rate for incomes above $1 million.

- A reinstatement of advance refunding rules (restoring the rules in place prior to the TCJA), which would likely increase the supply of tax-exempt munis compared with taxable munis. The supply could be substantial. Over the past year, muni borrowers have been issuing taxable munis at a near record rate — nearly $150B — in order to advance refund (refinance) older, higher coupon tax-exempt debt. This has been spurred by low overall interest rates, and, more importantly, the elimination of advance refunding as part of the TCJA.

- A reintroduction of Build America Bonds (BABs) or similar type of bond, which could change supply dynamics, potentially reducing supply of tax-exempt munis (BABs are taxable munis with a federal subsidy, and most were issued in 2009-2010).

The Bloomberg Barclays Municipal Bond Index is an unmanaged index of long-term fixed-rate investment-grade tax-exempt bonds.

The Bloomberg Barclays Taxable Municipal Bond Index is an unmanaged index of taxable municipal bonds traded in the U.S.

The Bloomberg Barclays AA Corporate Bond Index is an unmanaged index of Aa rated, fixed-rate, taxable corporate bonds.

BLOOMBERG® is a trademark and service mark of Bloomberg Finance L.P. and its affiliates (collectively “Bloomberg”). BARCLAYS® is a trademark and service mark of Barclays Bank Plc (collectively with its affiliates, “Barclays”), used under license. Bloomberg or Bloomberg’s licensors, including Barclays, own all proprietary rights in the Bloomberg Barclays Indices. Neither Bloomberg nor Barclays approves or endorses this material, or guarantees the accuracy or completeness of any information herein, or makes any warranty, express or limited, as to the results to be obtained therefrom, and to the maximum extent allowed by law, neither shall have any liability or responsibility for injury or damages arising in connection therewith.

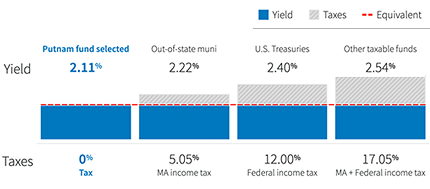

Evaluate yields on a tax-equivalent basis

Compare municipal funds on equal footing with taxable bond funds.

326069

More in: Fixed income