While target-date funds have offered an innovative investment vehicle, they are ripe for a new enhancement — personalization. Today’s target-date funds use age as their only input. By considering additional criteria and responding to evolving participant circumstances, asset managers can offer further target-date fund innovation. Importantly, benefits of personalization can be realized by all participants, including those defaulted into the QDIA or unengaged in their retirement saving. Working together, the plan sponsor, recordkeeper, and investment manager can share basic information to improve participant outcomes.

At Putnam, we believe personalization is the future, and we have built a personal target-date solution that:

- Leverages our existing, differentiated glide path

- Personalizes allocations to each participant

- Has demonstrated the ability to improve outcomes

Built on the Putnam Retirement Advantage strategy baseline

Our glide path philosophy, which is the foundation of everything we do in target-date investing, is to manage the right risk at the right time. We illustrate the Putnam glide path in Figure 1. It favors a larger equity weight than the industry average when there is a long horizon before retirement and losses can be recovered. The strategies then significantly reduce equity risk approaching the target date, when account balances are largest and recovery time is shortest. This is better for protecting near-retirement participants from retirement-endangering drawdowns. The target allocation at retirement seeks to balance risk between equities and fixed income.

Figure 1. Allocations of the Putnam target-date glide path versus the industry average

Sources: Putnam; Morningstar for industry average equity allocations; as of 3/31/23.

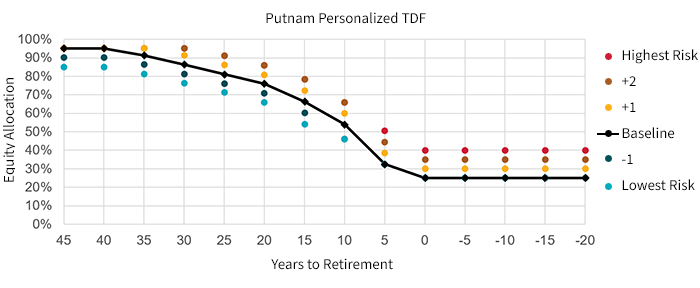

Our existing glide path serves as the baseline for the personalized solution available to participants, illustrated in Figure 2. Since our baseline begins with very aggressive allocations, our personalized target-date solution only needs the ability to adjust equity allocations lower at this point in the glide path. At the opposite end, our landing point is already theoretically optimal for maximizing risk-adjusted returns, so we do not need the flexibility to add fixed income, only to increase equity. In the middle of the glide path, personalized allocations are more symmetric around the baseline, and participant allocations can be adjusted up or down to reflect their individual retirement journey.

Figure 2. Personalization adjustments to Putnam target-date glide path

Source: Putnam.

Personalized for each participant

Personalization builds on the approach used in our existing target-date strategies by maintaining the focus on individual outcomes, and increasing the precision with which we do so. At Putnam, we believe portfolio value alone is not the best measure of retirement saving success, as this singular focus can lead to excessive risk taking for some participants. Delivering better outcomes relies on prioritizing two goals:

- Generate sufficient wealth to sustain retirement spending

- Focus on reducing variability of outcomes

While a traditional target-date strategy considers only participant age, personalization allows us to use additional variables. These variables, which are supplied automatically via a connection between the plan’s recordkeeper and a middleware provider, are:

- Age

- Income

- Account assets

- Participant savings rate

- Employer match

Without requiring participant action, Putnam uses a robust algorithm to calculate retirement savings progress for each participant and adjusts their allocation relative to the baseline, if necessary, to deliver a more appropriate portfolio.

Importantly, we are not simply creating parallel glide paths. Participant savings progress can be updated with any change to the underlying variables. This ensures that participant allocations dynamically respond to new information.

Pursuing better outcomes

Recall our dual objectives outlined earlier: to balance generating wealth with reducing variability of outcomes. We are excited to share that personalized target-date funds can improve the likelihood of achieving these objectives.

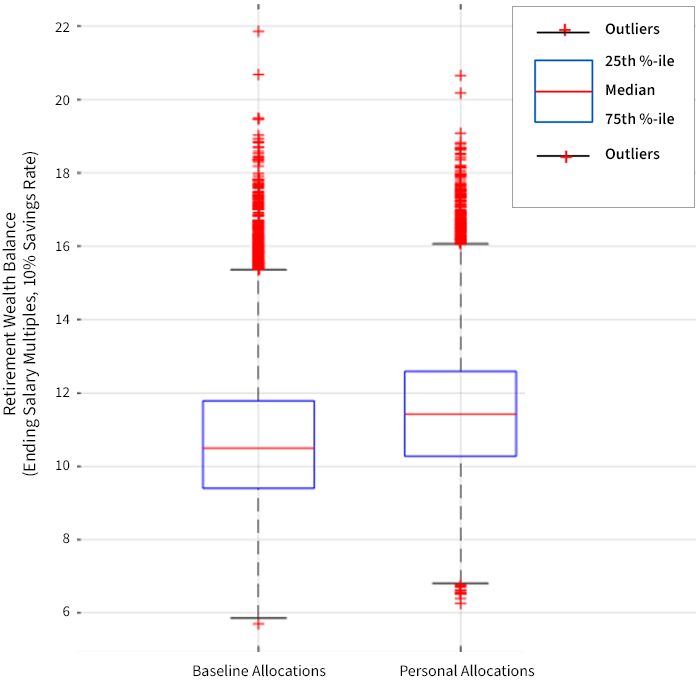

In Figure 3, we observe our personalized target-date solution delivers on the first objective, providing higher median wealth multiples at retirement. The red line, indicating the median wealth multiple at retirement, is higher in the case of the personalized target-date allocation. Importantly, though, personalization does not sacrifice objective two; it does not increase the variability of outcomes. The spread between the 25th and 75th percentiles, indicated by the blue boxes, is no wider with personalized allocations.

Note that one could increase median balances at retirement in any simulation by increasing equity. But simply increasing equity would also increase the variability of outcomes — potentially resulting in lower wealth balances in the bottom tail of the distribution. In keeping the distribution unchanged, yet still delivering higher median balances, we can directly see the powerful impact a personalized target-date solution could have. In fact, the median wealth multiple increases by approximately 1x ending salary, which, at 40% income replacement (net of assumed Social Security benefits), translates to 2.5 years of additional retirement income.

Figure 3. Personalizing target-date strategies can increase retirement wealth

Source: Putnam.

Conclusion

Age-only target-date funds have done an admirable job of improving participant allocations, and they likely have had the greatest positive impact on defaulted, unengaged participants. With improvements in technology, investment managers are able to deliver further innovation, personalizing this once groundbreaking idea — the target-date fund — to achieve even better participant outcomes. At Putnam, we’ve built a personalized target-date strategy that leverages our existing, differentiated glide path, personalizes allocations to each participant, and has historically demonstrated the ability to improve outcomes.

333764

More in: Asset allocation, Fixed income, Retirement,