In our view, the stability of stable value is a function of diversification and liquidity. For that reason, we believe it is worth taking a closer look at the structure of a given stable value strategy to determine the degree to which it possesses these two crucial characteristics.

Historically, a triad of underlying vehicles has formed the core of stable value, including traditional guaranteed investment contracts (GICs), insurance separate accounts, and synthetic GICs that rely on wrap contracts for book value accounting. But while each of these components has a legitimate diversifying role to play, only two of them — separate accounts and synthetic GICs — enjoy truly widespread usage today. In our view, to turn away from traditional GICs is to miss an opportunity to enhance the diversification and liquidity that stable value seeks to provide.

What is a traditional GIC?

A traditional guaranteed investment contract (GIC) is an investment contract issued by a AA- or A-rated insurance company or its affiliate. The buyer, or contract holder, pays the insurance company/issuer for the contract and those proceeds are then invested in its general account.

The interest rate — known as the crediting rate in the stable value context — may be fixed or floating and is based on the assets available for investment by the issuer as well as that issuer’s assessment of the risk associated with the plan(s) and the specific investment manager purchasing the contract.

The “guaranteed” portion of the name indicates that principal and interest are guaranteed by the insurance company. In other words, the guarantee is as good as the credit risk of the issuer. Stable value funds using GICs typically develop a diversified exposure employing a number of issuers.

The potential advantages of traditional GICs

GICs can provide a number of advantages to stable value portfolios. They offer stability and flexibility in the areas of credit risk and term structure risk, and, more importantly, they possess critical characteristics of liquidity, diversification, and crediting-rate enhancement.

Attractive structural credit risk

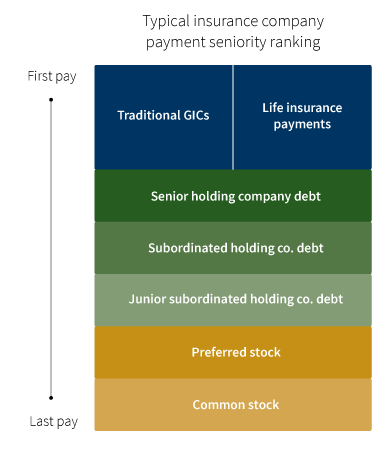

A GIC is a senior security in an insurance company’s capital structure. This means GICs sit at the top of the payment waterfall alongside life insurance policyholders.

Customizable term structure

Investors in traditional GICs are able to select principal, interest, and maturity payment dates for each GIC they purchase. This may be highly advantageous, particularly if the manager prizes liquidity as a key component of the overall stable value strategy.

Liquidity provisions

For the purpose of funding participant activity, traditional GICs are fully liquid due to their contractual provisions, which allow them to be “sold” back to the issuer at par.

Diversification potential

Traditional GICs offer exposure to a relatively stable investment vehicle backed by a long-tenured group of major U.S. insurance companies. With robust capacity parameters guiding their traditional GIC issuance, even modest GIC exposures can offer diversification benefits to investors.

Crediting-rate stability

Because traditional GICs do not fluctuate in price, they are insulated from duration risk. In this respect, traditional GICs are excellent crediting-rate stabilizers for synthetic GICs, which can fluctuate in value due to interest-rate changes and other factors.

Read our full investment insight, “Seeking to enhance the stability of stable value with traditional GICs.”

Risk considerations: Diversification does not assure a profit or protect against loss. It is possible to lose money in a diversified portfolio. A GIC represents the issuer’s agreement to make interest and principal payments in the amounts and at the times specified by the contract. Investment contracts typically pay an interest rate (also referred to as the crediting rate) that adjusts periodically on a specified schedule. These contracts allow a constant valuation of the contract at book value, but the crediting rate will increase or decrease based on changes in the market value of the underlying securities and the interest paid on the securities. The payment of principal and interest of a GIC contract is dependent on the creditworthiness of the issuer. In the event of a default on its obligations by a GIC issuer, the owner could incur a loss of principal. The creditworthiness of investment contracts is dependent on the financial health of the relevant wrap providers or investment contract issuers. The contract reserves for GICs are held in the insurer’s general account, and the ability of the insurer to meet its contractual obligations ultimately depends on its financial stability. GICs are not insured by any federal agency.

304014

More in: Fixed income,