- The perception of more attractive equity valuations outside the United States can be attributed to differences in industry group weightings of regional indexes, our analysis indicates.

- We believe current price-to-earnings multiples are not a reason to avoid U.S. equities, nor are valuations alone a reason to favor other regions.

- A selective approach across markets is more likely to identify undervalued opportunities than an index valuation approach.

As a follow-up to a perspective we wrote in November, we would like to expand the comparison of U.S. equity valuations to other regions. Our aim is to counter the narrative that U.S. equities are quite expensive and that better value can be found elsewhere. While our primary focus as active investors is on stock-specific research, we find that the power of this narrative deserves a closer look. In our analysis, we believe that regional valuation disparities disappear when differences in index sector weightings are reconciled.

How do valuations compare across the five major investment regions?

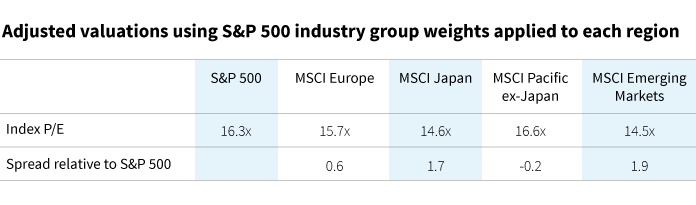

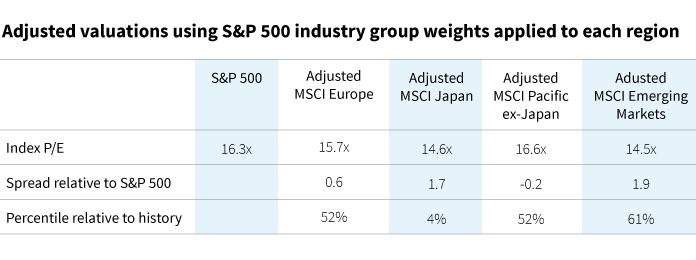

On the surface, U.S. stocks appear more expensive than non-U.S. stocks. The U.S. market (S&P 500 Index) with a P/E of 16.3x expected next-twelve-month earnings as of March 31, 2018, is pricier than Europe (MSCI Europe Index), Japan (MSCI Japan Index), the Pacific region excluding Japan (MSCI Pacific ex-Japan Index), and Emerging Markets (MSCI Emerging Markets Index). In these non-U.S. indexes, P/Es currently range between 12.3x to 14.9x.

Large differences in industry group composition across regions

We find that the difference in industry group weights drives much of the difference in regional P/Es shown above. The S&P 500 has more weight in industry groups with higher price multiples, such as software & services, and less weight in lower multiple groups such as automobiles.

When we normalize for industry group differences by applying S&P 500 industry group weights to the other indexes, the valuation spread of other regions relative to the United States shrinks. Under the adjustment, all regions outside the United States trade within 2.0 P/E of the S&P 500.

The historical dimension shows a significant change

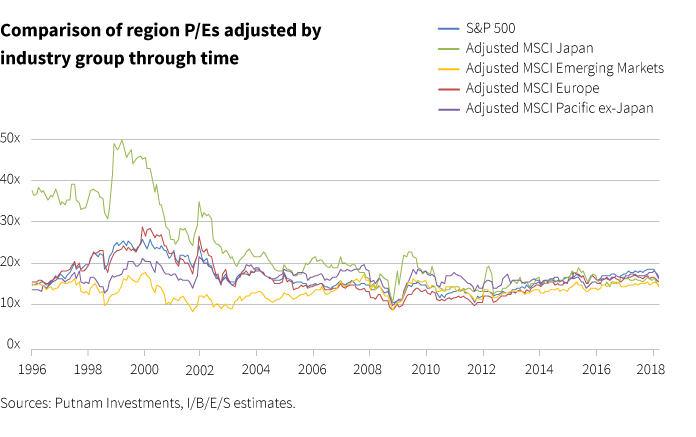

We can plot the regional P/Es measured on the same industry group basis back through time. We see that region-adjusted P/Es today trade in a much tighter range relative to the past when emerging markets traded at more of a discount and Japan traded at more of a premium.

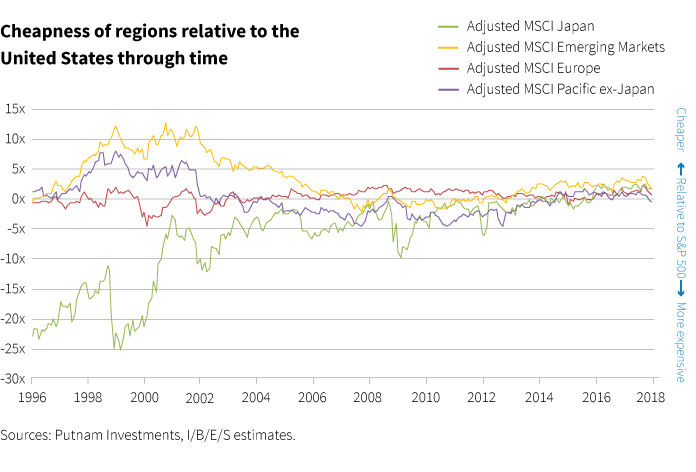

To put this data into a broader context, we can measure how cheap or expensive other regions’ adjusted valuation levels are relative to the United States historically. Certain regions may trade at a structurally higher or lower valuation level given differences in expected risk, growth in earnings, and political stability.

When compared with measurements of the past 22 years, recent valuations of benchmarks representing Europe, Pacific ex-Japan, and Emerging Markets all fall within a normal range relative to the United States. Japan, on the other hand, looks inexpensive today, as it has typically traded at a higher multiple than the United States over the 1996 to 2018 period.

Below is a plot of P/E spreads offered by each industry group-adjusted region P/E in excess of the S&P 500 P/E. From this vantage point, Japan looks cheap relative to the United States, with the other regions looking comparable to how they have been valued relative to the United States in the past.

The role of risk and interest rates

Some of the convergence in regional P/E spreads is due to changes in perceived risk. Credit default swaps (CDS) are a proxy for a country’s risk level. CDS levels have decreased for emerging-market countries relative to where they were 15 years ago.

Conversely, Japan’s long-standing P/E premium can partly be explained by extremely low interest rates relative to the rest of the world. Japan’s discount rate has been below 1% for more than 20 years (Source: FRED.stlouisfed.org). The convergence of Japan’s P/E multiple to more global norms is therefore partly a function of convergence of global interest rates to similar extremely low levels through synchronized quantitative easing by central banks.

It’s about more than multiples

This analysis shows that simple region P/E analysis misses the point. It does not take into account industry group composition effects or view how current valuation differentials fit into a historical context.

Seeking broad exposure to a region as a whole based on valuation levels may be misguided. Such an approach, without closer stock-by-stock analysis, could lead to a “value trap” — a strategy that erroneously favors stocks with low multiples, but which continue to underperform nonetheless, often because earnings fall short of expectations. That’s not to dismiss other regions with a broad brush; Putnam’s fundamental research has uncovered many attractive opportunities among regions today.

Quantitative Analyst Brian Hutter, CFA, contributed to this research.

311372

More in: Equity, International,