Two weeks after Election Day, we believe the markets have a lot more clarity. From a political standpoint, former Vice President Biden has secured enough electoral college votes to be named president-elect and the Democrats have retained control of the House of Representatives. From a pandemic standpoint, data from two vaccine trials so far have been extremely positive.

Despite these developments, some uncertainties remain: the lack of a concession from President Trump, and which party will control the Senate, an outcome to be determined by two run-off elections in Georgia. In our opinion, both of these uncertainties are currently being priced in volatility markets:

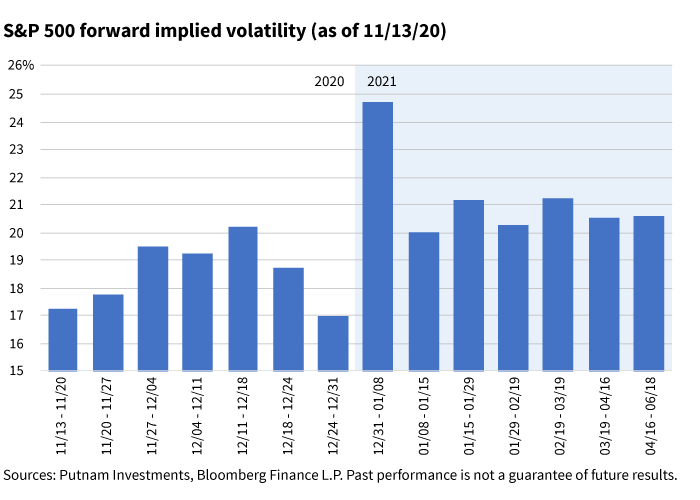

Looking at the forward implied volatility from S&P 500 options contracts gives us a granular look at how the market is pricing risk on a weekly basis. From the chart above, we can see two implied events in the immediate future: one during the week of December 11–18, 2020, and one during the week of December 31, 2020–January 8, 2021. The small risk event (The S&P 500 Index is an unmanaged index of common stock performance.

324100