Continued weakness in energy prices is expected for the second half of 2015, largely due to a supply and demand imbalance in the oil market.

After two quarters of relative stability, commodities have again entered a period of renewed volatility. Demand has further weakened on fears about the meltdown in the Chinese stock market. At the same time, energy supplies remain high.

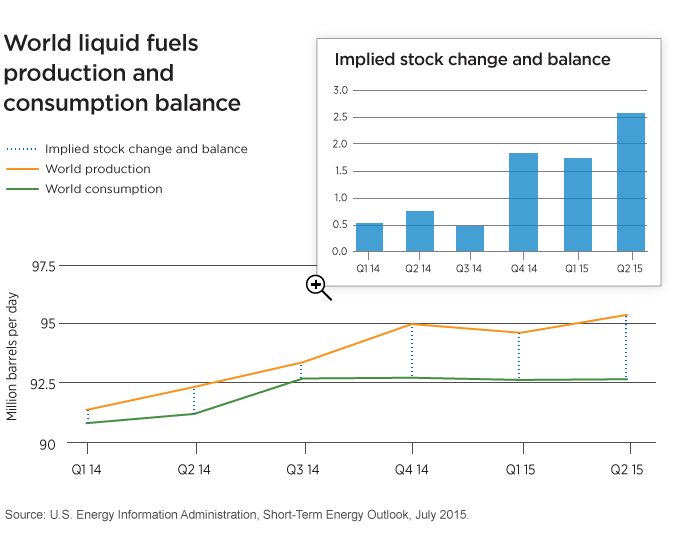

When oil prices plummeted in the second half of 2014, producers in North America decided to reduce rig counts, with the expectation of lower output. Instead, the production declines never materialized because only marginal wells were scaled back, while production costs at operating rigs have continued to decline due to technology advances. Consequently, North American production merely plateaued at an elevated level while OPEC and other non-OPEC production continued to climb.

While energy consumption had been relatively stable in the developed world, supply has continued to expand.

In addition, some optimism around the recent Iran nuclear talks indicated the potential to lift that country’s oil export sanctions, creating the possibility of a new round of selling across the commodity complex.

A quick resolution to these issues is not expected and, in our view, an underweight position in commodities overall is warranted.

Read more about Putnam’s current thinking in Capital Markets Outlook.

296186

More in: Macroeconomics