Stagnant wages in the fourth quarter could drive the Fed to rethink its policies.

Wage growth has been missing from the U.S. recovery since 2009. A debate rages about whether this reflects the generally weak characteristics of this cyclical recovery or a structural problem in the labor market. According to the latter theory, U.S. companies are generating job openings, but there are too few workers with the right skills to fill them.

The recovery is strong enough, in our view, to resolve this debate. Our analysis of the relationship between the unemployment rate and wage growth (our take on the traditional Phillips curve) suggests that wages should begin rising when the unemployment rate crosses a threshold of 6.5%. Coincidentally, when the Fed originally launched QE3, it named 6.5% as the rate at which it would remove “emergency” measures.

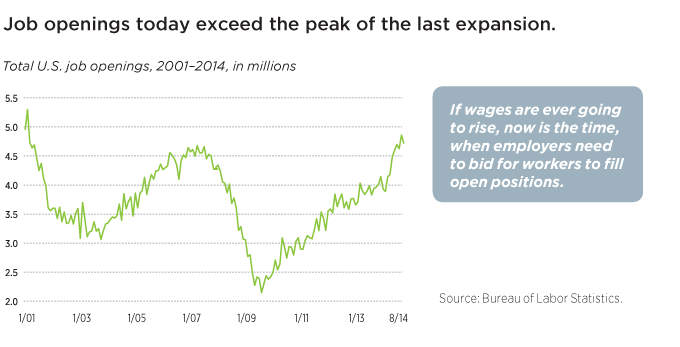

U.S. unemployment dropped to this rate in the first half of 2014, and has since fallen below 6%. In addition, the JOLTS (Job Openings and Labor Turnover Survey) data of the Bureau of Labor Statistics show that there are more unfilled jobs today than at the peak of the last expansion in 2006 and 2007.

If wages are going to rise during this expansion, now is the time, when employers need to bid for workers to fill open positions. If wages continue to languish, then something is wrong with the Fed’s traditional models and assumptions.

Read the full Putnam Capital Markets Outlook.

291567

More in: Asset allocation