A trending idea among the more apprehensive analysts of U.S. economic growth is that the financial crisis of 2008 somehow crippled the economy for the long term.

We find this pessimistic outlook to be unsupported by fact. Our research suggests that a return to longer-term historical growth trends is more than possible; we think it’s the most likely scenario for the near term.

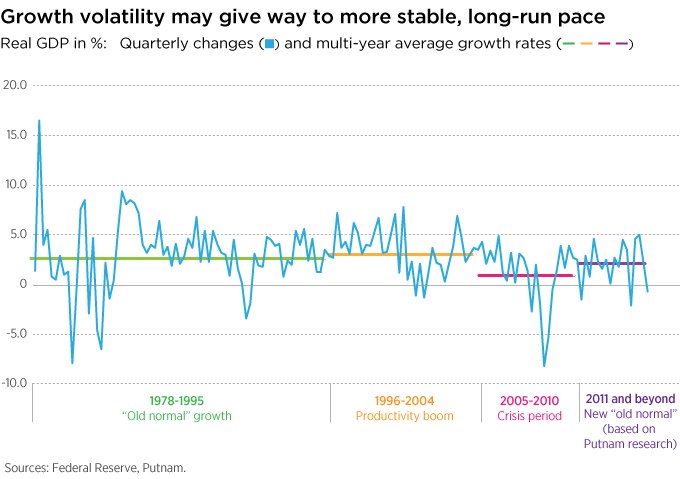

Interpreting quarterly economic contractions and expansions

Our forecast for long-term U.S. growth is 2.2%. This may seem a bit unexciting next to the 4.6% and 5.0% GDP growth rates during the second and third quarters of 2014, respectively. But, we observe, the quarterly GDP prints for the full year of 2014 illustrate a pattern of contraction and expansion: -2.1%, +4.6%, +5.0%, and +2.2%. Despite the weather-induced negative GDP print in the first quarter of 2015, we think the result in 2014’s fourth quarter heralded the return of the “old normal” rates that pre-date the financial crisis.

The long-run, steady pace

As the U.S. economy has passed from recession to recovery, growth has acted like a spring: When it was depressed, the spring contracted and was much smaller than when it was at rest, or in a neutral state. Conversely, when the spring was released, it expanded rapidly, becoming much bigger than when it was in a neutral state. But all things being equal, the spring eventually returns to its neutral state — or, in the case of GDP, it returns to its longer-run, steady pace.

Overall GDP growth for 2014 was 2.4%, closer to our long-run estimate, though admittedly this is merely a short-run example used to illustrate the point. Interestingly, the conditions that contribute to our long-range forecast of 2.2%, particularly a factor known as “total factor productivity” (or TFP) — a measure of innovation and efficiency-enhancing elements at work in the economy — reveal an internal dynamism of U.S. growth that most observers have tended to overlook.

Financial professionals: Read Putnam’s latest research, The “old normal” returns, for more on the outlook for U.S. GDP growth.

295616

More in: Macroeconomics