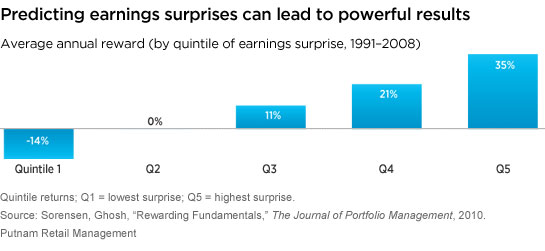

Successfully predicting big earnings surprises — and avoiding the largest negative-surprise stocks — can carry big potential rewards. Two researchers at PanAgora Asset Management demonstrate how. Breaking down the broad stock market (as measured by the Russell 3000 Index) into quintiles of earnings surprise between 1991 and 2008 shows that stocks with the largest positive year-over-year earnings increases relative to their forecasted earnings at the start of the year tended to perform dramatically better than stocks with negative earnings surprises.

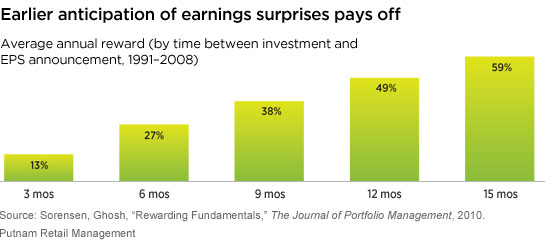

Finding an earnings surprise early, before the surprise becomes a known quantity, can yield additional returns. The potential rewards increase with the length of the forecast horizon.

Accurate forecasting of the biggest positive earnings surprises twelve months in advance, for example, would deliver a much higher return than making the same forecast only three months in advance of the relevant earnings announcements. Said another way, having an insight too late can dramatically reduce an opportunity’s reward potential.

Read more in our paper:

Independent equity research: How we do it, and why it matters to investors

More in: Equity