- Municipal bonds outperformed treasuries and the broader taxable bond market in Q3

- Additional state and local aid has to wait until after the November elections

- We continue to see many opportunities in lower-rated municipal bonds

The recovery in the municipal bond market continued in the third quarter as munis outperformed U.S. Treasuries and the broader taxable bond market.

A number of factors strengthened confidence in the muni market, including the expectation of more pandemic relief for states and the Federal Reserve’s view that short-term rates would remain near zero for some time.

Demand remains steady

Widespread expectations that Congress would soon pass an additional pandemic relief bill — including more aid for state and local governments — helped buoy investor confidence in municipal bonds in the course of the third quarter. Although state revenues have been negatively impacted due to COVID19, recent data indicate the decline hasn’t been as steep as was expected this past spring. As a percentage of outstanding municipal bonds, default rates have averaged less than 0.25% over the past decade (Moody’s annual default report, 2020).

In our view, most states coming into the pandemic were in the best financial condition they have been in over a decade. Many states had ample cash reserves. Other states, less prepared, have the financial flexibility to navigate budget gaps. Additional aid could further strengthen state budget situations as the pandemic and recession continue to weigh. Although Congress and the White House could not reach an agreement in either September or October, we believe direct aid to states and municipalities remains warranted and necessary.

As we look at fundamentals, we are optimistic about revenue projections as more data comes in. It appears that revenue may be down 5% year over year,* which is significant, but less than originally anticipated. Also, real estate taxes represent the highest source of revenue for local governments. On average, property values are up 4% year over year and 3% year to date.* That bodes well for this revenue source.

Downgrades have risen across the municipal landscape, though we believe the majority of borrowers will be able to weather the pandemic.

The Fed’s expectation to keep short-term rates near zero through the end of 2023 has also been supportive. With interest on certificates of deposit and Treasuries near zero, investors have sought alternatives. Although municipal bond yields were near historic lows, their relative after-tax income advantage has remained compelling.

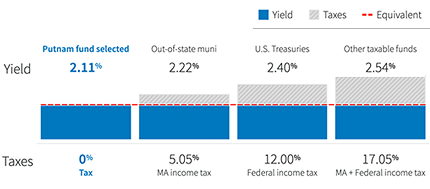

Evaluate yields on a tax-equivalent basis

Compare municipal funds on equal footing with taxable bond funds.

Opportunity in credit markets

We believe the lower tiers of the investment-grade market and parts of the high-yield market currently represent some of the best income and return opportunities. Spreads are at their widest point in nearly six years. On the credit spectrum, higher-yielding, lower-rated municipal bonds have outpaced higher-rated municipal bonds in recent months.

Relying on a deep bench in credit research, we are identifying opportunities in states, utilities, charter schools, tobacco, and other sectors. On the state side, we continue to favor a few states, including Illinois, while avoiding Puerto Rico.

The path ahead remains unclear due to the uncertain course of the pandemic and post-election uncertainty, but there are encouraging signs for the economy. Activity has picked up from depressed levels thanks in part to a vibrant housing market and an uptick in business investment. However, while unemployment has continued to decline, it remains at a level that could restrain state and local tax revenues.

*Source: “State finances bolstered by cash reserves, housing market,” (video), G. Hamilton, Putnam, 2020.

Financial professionals (login required): Join our November 10 webcast, “Municipal Bond benefits post-election.”

323901

More in: Fixed income