- Growing in number, Millennials are having a significant influence on plan design

- Younger cohorts have different financial challenges than other generations

- Think systematically about workplace savings, financial wellness, and education

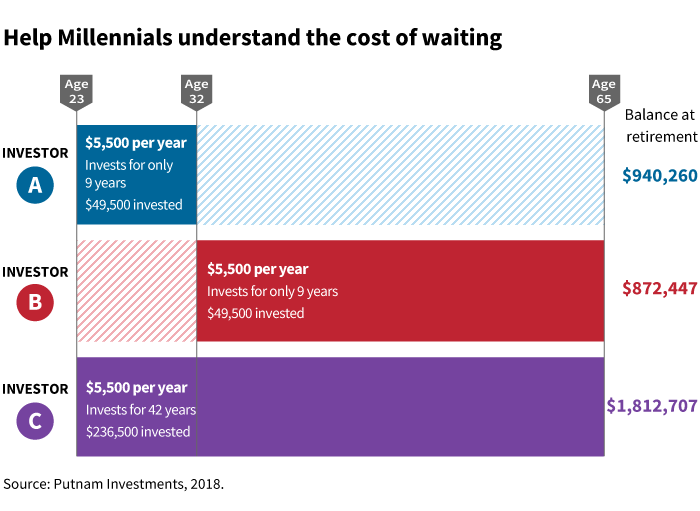

Millennials are saving earlier and at a higher rate than previous generations. But it’s not yet time to signal the all clear for twenty- and thirty-somethings when it comes to retirement saving success. Obstacles in place such as college debt, investment choices, and lack of access to workplace savings plans may cause them to lag in meeting their ultimate goals.

According to the Transamerica Center for Retirement Studies:

- Millennials began saving earlier than other generations, at a median age of 24

- On average, Millennials participating in a 401(k) are saving 10% of income

The good news is that time is on their side.

This generation represents the largest segment of the workforce (Pew Research). Millennials’ economic sway creates an opportunity for plan sponsors and advisors to influence their saving success.

Plan design — a proven driver of investor behavior and retirement readiness — is a good place to start.

What sponsors and advisors should think about

As Millennials have grown in number, their needs have begun to shape plan design, much like Boomers did in decades past. It may be time to evaluate whether the retirement plan you offer, or advise, serves multiple age groups well.

- Review design features. Automatic features such as auto-enrollment, auto-QDIA (offering a qualified default investment alternative), and auto-escalation of contributions may be popular among participants who like to take advantage of opportunities to automate tasks. Modeling these changes’ impact on the plan’s overall success score can add credibility to those design choices.

- Seek solutions with enhanced technology. Millennials have grown up with devices. Optimizing workplace plan interactions for devices will have a positive response, and one that may benefit all generations. While not native to Boomers, use of mobile devices and adoption of online banking services has grown significantly. A Gallup survey found that 71% of Boomers bank online at least once per week. Pew Research noted that 68% of Boomers and 90% of Gen Xers own smartphones. Tablet ownership is about the same across most generations.

- Address financial wellness. Millennials face different challenges than other generations. Workplace programs can help them manage the stress that results. Millennials face a greater college debt burden, lower career earnings due to delayed career starts, rent inflation, and health-care cost inflation. All of these factors can make it difficult to save.

More employers are paying attention to the causes of employee stress and are offering financial wellness initiatives.

Most workers (75%) believe that financial wellness programs are a key benefit (Morgan Stanley). Many employers on average offer several different financial wellness programs.

Investor education can play a role in wellness programs. Illustrating the power of saving for the long-term can be a powerful message for young savers.

Build a plan for all ages

Offering a robust, finely tuned 401(k) plan can help recruit or retain talent, too. Just over half of Millennials (55%) have access and are eligible to participate in workplace savings plans. Studies have shown that, with access to a plan, 94% of Millennials will save for retirement (National Institute on Retirement Security, 2018).

At the same time, average account balances are not soaring. What’s holding Millennials back?

Lack of access to workplace savings, eligibility requirements, and investment choices may slow the pace of saving for Millennials.

Several studies show that Millennials tend to avoid investing in stocks due to risk. A recent Bankrate survey found that only 23% of those aged 18 to 37 believe the stock market is the best place for a long-term investment. Among Millennials, 30% said they preferred an allocation to cash.

To improve investment choices, evaluate plan offerings and consider target-date funds, which are popular due to their simplicity. Another strategy that appeals to Millennials is sustainable investing. A recent study found that 95% of Millennials are interested in ESG and impact investing (Morgan Stanley, 2019).

Developing communications focused on “Total Rewards” can help employers tout their entire benefits package. Total rewards describes all the tools available to an employer to attract, motivate, and retain employees.

Recruiting and retaining a workforce, and helping them achieve retirement success is as difficult as these tasks have ever been. Making a retirement plan appealing to multiple generations may help attract and retain workers in a tight labor market. Working teams of diverse ages might also be better able to solve problems for the company. As an employer with its own multigenerational workforce, Putnam is here to help.

319568