Since 2009, we have warned that the Barclays Aggregate indexes (the U.S. Agg and the Global Agg), which serve as benchmarks for trillions of dollars of investors’ money invested in mutual funds and other vehicles, represent a diminished set of opportunities for fixed-income investors.

Our view continues to be that more attractive forms of risk can be found outside these indexes.

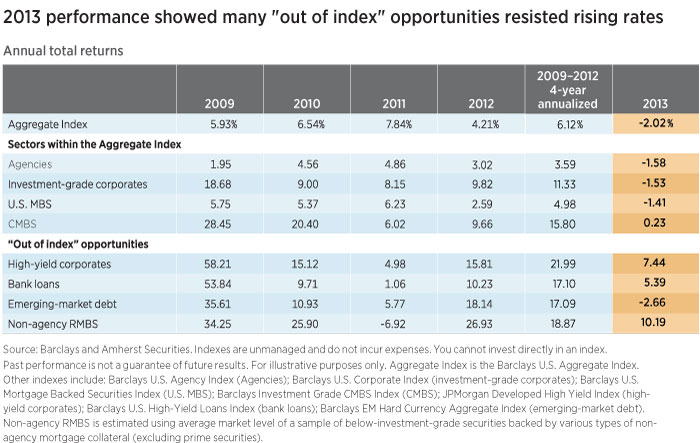

Performance history supports our view

While Agg-benchmarked products and generally longer-duration portfolios avoided poor results in the first four years after the financial crisis, the true risk of the Agg’s composition began to emerge in 2013. With interest rates coming unmoored from their historic lows, our thesis on the Agg — especially our focus on its vulnerability to interest-rate risk — began to prove itself out, particularly after the U.S. Federal Reserve began to discuss “tapering” its bond-purchase program.

Performance records compared: in and out of the index

In the years since the financial crisis, spreads in various fixed-income sectors, both within the index and outside it, have tightened dramatically from their historically wide levels, retracing much of the widening that occurred in the 2008–2009 period. Of course, spread compression during this period led to historically large returns for virtually all fixed-income asset types.

But as the table above shows, 2013 marked a watershed moment for index versus non-index sectors in fixed income. With the exception of emerging-market bonds — which, during the second half of 2013, experienced a strong downdraft due to foreign investor outflows amplified by currency weakening — out-of-index opportunities soared while the Agg and many of its components suffered. In 2013, the Barclays U.S. Aggregate Index delivered a return of -2.02%, marking the first calendar year that the index was in negative territory since 1994.

Index-related risk may be an emerging trend

We fear this could become a recurring theme over the next few years if interest rates should embark on a sustained rise, as we expect them to. This could be the case until we return to a more “normalized” world in which investors are compensated with higher yields given the level of interest-rate risk (duration) they are taking.

290764

More in: Fixed income