- Millennials are 50% more likely than Gen-Xers to save more than 5% of their paycheck (Source: Bankrate)

- However, millennials are using taxable savings accounts for their retirement savings in greater numbers than older workers do

- The majority of millennials cite lack of availability as the reason for using a bank account rather than a qualified plan

Younger workers are saving for retirement, but they may be missing out on the tax advantages of a qualified plan.

While employer-sponsored defined contribution plans or individual retirement accounts (IRAs) offer tax incentives to save, the majority of adults in a recent survey — 55% — reported that they use a regular savings account to save for retirement. Among millennials — those between the ages of 18 and 34 — that percentage rises to 63%.

Just 50% in the NerdWallet/Harris Poll of some 2,000 adults stated that they use a workplace retirement plan such as a 401(k), and 39% also use IRAs.

Access to a workplace savings option is not universal

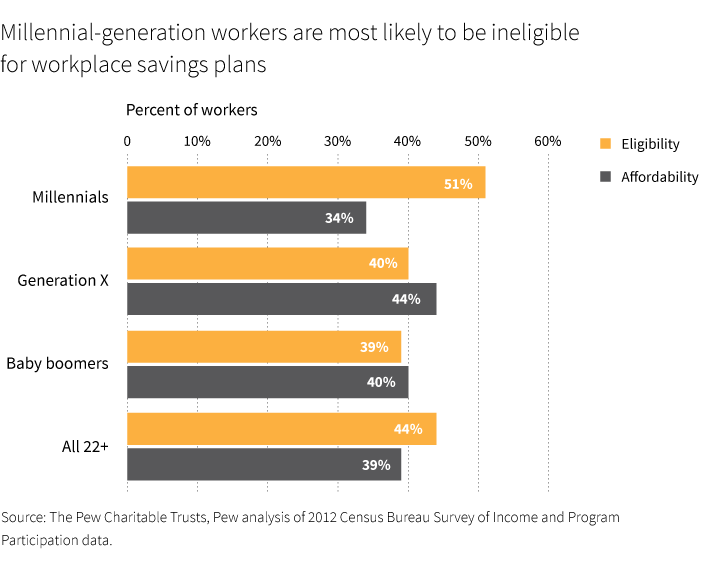

Older workers participate in 401(k) plans at higher levels than millennials and largely for the simple reason that older workers have greater access to such plans. According to worker surveys conducted by the Pew Charitable Trusts, more than half of millennials (51%) cite ineligibility as the reason that they do not participate in a workplace savings plan. Among the baby boom generation, only 39% of workers report this reason as a hindrance to savings.

The type of work millennials find can make a difference. New college graduates may have a difficult time finding a job with retirement benefits, or they may be working in part-time jobs and logging fewer hours than required to qualify for benefits. Many also do freelance work, which typically does not provide access to a 401(k). For those who find a job with benefits, there may be a waiting period for new hires. Also, workplace plans without auto-enrollment features may be letting younger workers slip through the net.

Affordability is another issue. But even accounting for income, millennials are less likely to participate in a 401(k) than boomers, Pew found.

The predicament millennials face may be one reason why, today, there are 43 million workers nationwide without access to workplace savings (Source: Bureau of Labor Statistics, 2016).

Employer match can make a big difference

Across all generations, participation in a 401(k) plan increases when plans include matching contributions from employers, Pew’s research noted. In plans with an employer match, 81% of millennials and 80% of boomers participate. Without a match, only 56% of eligible millennials participate, compared with 74% of boomers.

307605

More in: