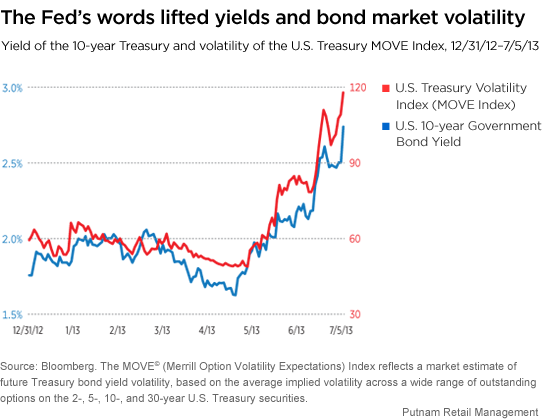

The Fed’s comments in May and June about reducing its asset purchase program generated significant interest-rate volatility in the United States, changing the opportunity set for fixed-income investors. Spread sectors — meaning sectors that trade at a yield premium to U.S. Treasuries — that had been buoyed by the massive liquidity created by the Fed’s purchases, sold off in June, with emerging-market bonds getting hit particularly hard. Global government bonds also fell, although not to the same degree as sectors with greater risk.

Despite the rapid increase in yields, we believe the broader U.S. economic recovery remains on track and should continue at a moderate pace, as recent data have been a bit better than expected. We also believe that the U.S. housing recovery will continue apace, although mortgage rates moved higher during May and June. In our view, home sales are improving because of stronger economic activity and better consumer confidence, not because of mortgage rates. In mortgage credit, following the liquidity-driven sell-off, we have found opportunities more attractive in non-agency residential mortgage-backed and commercial mortgage-backed securities.

As investors adjust their expectations about when the Fed will actually begin tapering its asset purchases, we expect continued volatility in interest rates and yield spreads. However, we think it’s unlikely that they are going to suddenly spike dramatically higher. As a result, we believe the environment for corporate credit and other risk-based fixed-income categories may continue to be favorable.

More in: Fixed income, Outlook