Emerging markets are vulnerable to the marginal tightening of U.S. monetary policy, we believe, caused by the reduction in bond purchases by the Fed. In December, the Fed announced it would reduce its $85-billion-per-month bond-purchase program by $10 billion beginning in January. Although the Fed describes the reduction as less accommodation — rather than marginal tightening — we believe the impact is likely to weigh on economic growth in emerging markets. Although these markets should continue to show positive GDP growth, they are not likely to be the primary drivers of global growth in early 2014.

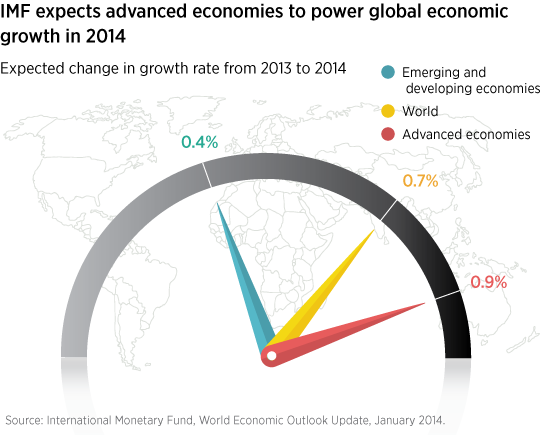

The IMF World Economic Outlook published in January 2014 anticipates that GDP growth in emerging and developing markets, though at a higher level than advanced markets, is likely to grow at a relatively slower pace during 2014. After falling from 4.9% in 2012 to 4.7% in 2013, growth in emerging markets should rise to 5.1% in 2014. By contrast, the IMF sees advanced economies moving from a 1.3% growth rate to 2.2%, helping to lift the world from a 3.0% growth rate to an expected 3.7% rate in 2014.

Countries with high current account deficits and those reliant on external financing will be hardest hit. In addition, currencies of countries with weak external trade balances, such as Indonesia, India, Turkey, and South Africa, are vulnerable.

However, a deceleration in emerging-markets growth is unlikely to drag down developed markets, in our view. The United States, Japan, and Europe can all be engines of global growth in 2014.

Read more in Putnam Capital Markets Outlook.

286333

More in: Asset allocation, Outlook